HECM vs. Proprietary Reverse Mortgage for Purchase

Which Reverse Mortgage Purchase Option May Be Right for Your Next Home?

Buy the Home You Want While Conserving More of Your Retirement Assets

Local. Trusted. Committed since 1986.

Many retirees want to purchase a new home without taking on a traditional monthly mortgage payment. A Reverse Mortgage for Purchase may provide an opportunity to buy a home while using a portion of your retirement assets as a down payment and financing the remaining balance with a reverse mortgage.

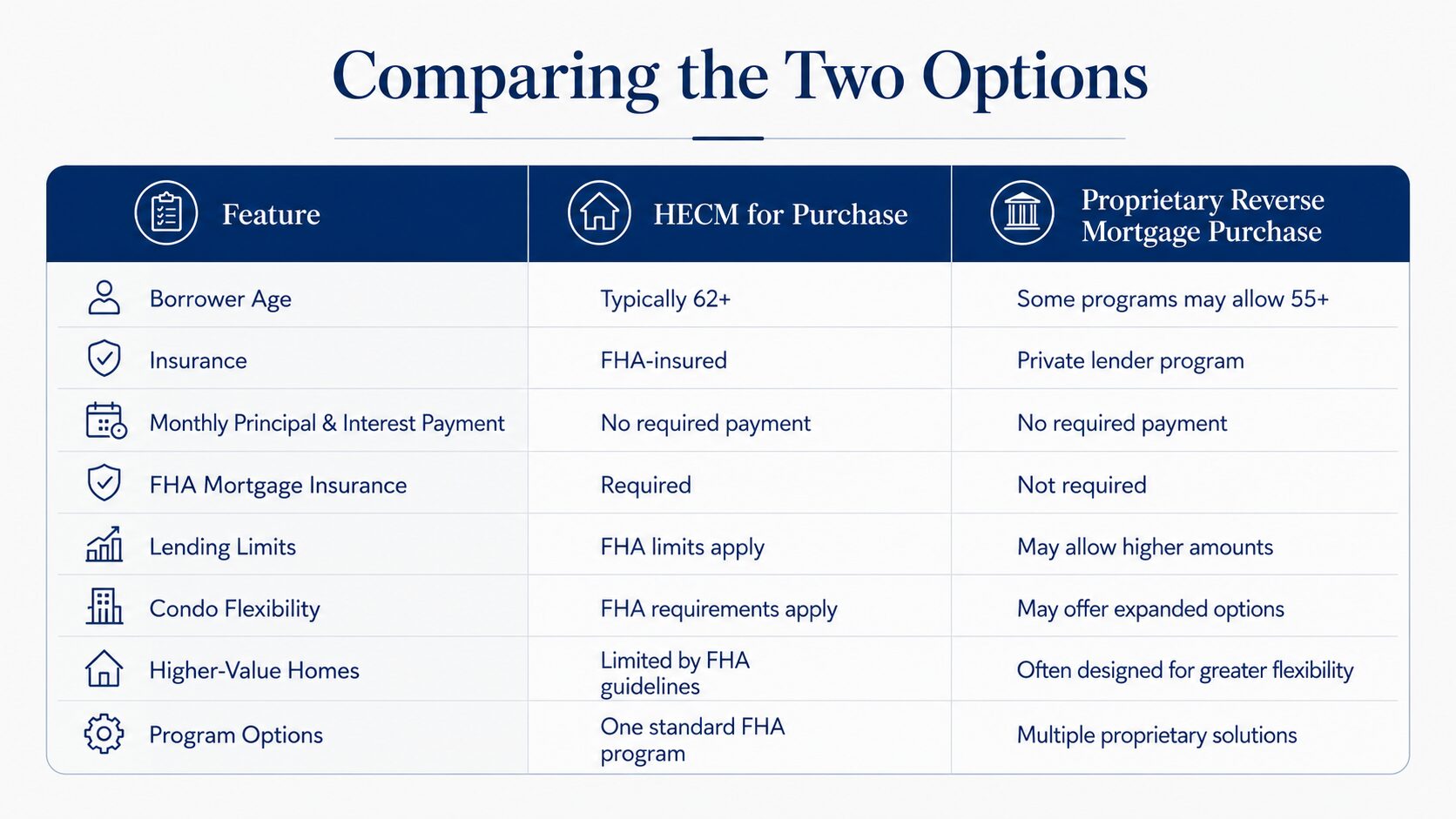

Mortgage South of Tennessee offers both:

• FHA-insured HECM for Purchase

• Proprietary Reverse Mortgage Purchase Programs

Each option has unique advantages depending on your home price, retirement goals, financial resources, and long-term plans.

Let’s compare a hypothetical example:

Scenario: 70-Year-Old Tennessee Homebuyer

Home Purchase Price: $550,000

Borrower Age: 70

Primary Residence: Tennessee

Goal: Purchase a new home without a required monthly principal and interest mortgage payment

(Example figures only. Actual qualification, proceeds, and costs vary based on program guidelines, interest rates, borrower qualifications, and lender approval.)

Option 1: FHA HECM for Purchase

Traditional FHA Reverse Mortgage Purchase Option

A HECM for Purchase allows qualified homeowners age 62 and older to purchase a new primary residence using a reverse mortgage.

Example Scenario:

Purchase Price: $550,000

Estimated HECM financing:

- Reverse mortgage proceeds: approximately $280,000 – $320,000

- Borrower contribution/down payment: approximately $230,000 – $270,000

- Monthly principal and interest mortgage payment: $0

(Illustration only. Actual proceeds depend on current FHA guidelines and borrower qualifications.)

Potential Advantages of a HECM for Purchase:

- FHA-insured program

- Government-backed borrower protections

- No required monthly principal and interest mortgage payments

- Ability to preserve some retirement assets

- Available nationwide through FHA-approved lenders

Considerations:

- FHA lending limits apply

- FHA mortgage insurance premiums apply

- Property must meet FHA eligibility requirements

- Condominium approval requirements may be more restrictive

Option 2: Proprietary Reverse Mortgage for Purchase

More Flexibility for Today’s Homebuyers

Proprietary reverse mortgage purchase programs are privately funded alternatives designed to provide additional flexibility beyond traditional FHA limits.

Depending on the program, they may offer advantages for borrowers seeking:

- Different age eligibility options

- Higher-value homes

- More flexible property guidelines

- Expanded condominium options

- Customized reverse mortgage solutions

Example Scenario:

Purchase Price: $550,000

Estimated Proprietary Reverse Mortgage financing:

- Reverse mortgage proceeds: approximately $330,000 – $390,000

- Borrower contribution/down payment: approximately $160,000 – $220,000

- Monthly principal and interest mortgage payment: $0

(Illustration only. Actual terms vary by proprietary program, lender approval, interest rates, and borrower qualifications.)

Why Some Buyers Choose a Proprietary Reverse Mortgage

A proprietary reverse mortgage may be worth considering if you:

Want to Reduce Your Cash Investment

A higher reverse mortgage advance may allow you to use less of your retirement savings for the purchase.

Want More Property Flexibility

Some proprietary programs may provide options for condominiums or properties that do not fit traditional FHA guidelines.

Want More Reverse Mortgage Choices

Every homeowner’s retirement strategy is different. Having multiple programs allows us to compare solutions rather than forcing every borrower into one option.

Example: Preserving Retirement Assets

Consider the difference:

Traditional Purchase

$550,000 Home Purchase

• $550,000 cash purchase or traditional mortgage financing

• Potential monthly mortgage payments

• Greater impact on retirement savings

Reverse Mortgage Purchase

$550,000 Home Purchase

• Use a portion of retirement assets for required contribution

• Finance remaining balance through reverse mortgage

• No required monthly principal and interest mortgage payments

• Keep more retirement assets available for other goals

Who May Benefit from a Reverse Mortgage Purchase?

A Reverse Mortgage Purchase may be a good option for homeowners who:

✔ Are downsizing or relocating

✔ Want to move closer to family

✔ Prefer a newer or lower-maintenance home

✔ Want to avoid monthly mortgage payments

✔ Have retirement savings they want to preserve

✔ Want to maximize financial flexibility

Why Choose Mortgage South of Tennessee?

For nearly 40 years, Mortgage South of Tennessee has helped homeowners make informed decisions about their reverse mortgage options.

Our reverse mortgage specialists provide:

✔ Access to HECM and proprietary reverse mortgage programs

✔ Personalized comparisons based on your goals

✔ Experience with Tennessee homeowners

✔ Education before application

✔ Guidance throughout the entire process

We believe the best reverse mortgage decision starts with understanding your options.

Find Out Which Reverse Mortgage Purchase Option Fits Your Retirement Goals

Whether a HECM for Purchase or a proprietary reverse mortgage is the better fit, Mortgage South of Tennessee can help you compare your choices.

Schedule your complimentary consultation today.

Mortgage South of Tennessee

Local. Trusted. Committed since 1986.

Important Disclosure

A reverse mortgage is a loan secured by your home. Borrowers must continue to meet loan obligations, including paying property taxes, homeowners insurance, applicable HOA dues, maintaining the property, and occupying the home as their primary residence. Loan proceeds, eligibility, costs, and available programs vary based on borrower qualifications, interest rates, property value, lender guidelines, and program requirements. This example is for educational purposes only and is not a commitment to lend.